Marketing Case Study: Pharmaceutical Price Points – Pricing the EpiPen

Todd Benschneider – University of South Florida – Dr. James Stock

June 29, 2017

Introduction

Mylan Pharmaceuticals gained front page notoriety in 2016 for its part in sweeping allegations of price gouging and Medicaid abuses among large pharmaceutical companies. Consumer backlash to the rising costs of healthcare fueled a hailstorm of media attention, spotlighting Mylan’s unprecedented price inflation of several older generic drugs. The Mylan product at the forefront of the debate was the EpiPen; an emergency treatment device that assists patients in self-administering adrenaline (epinephrine) during severe allergic reactions. The device had grown into a household brand over the 30 years since its introduction and EpiPen’s brand loyalty provided the foundations for one of the industry’s most successful, and now most questionable, brand revitalization campaigns ever launched. The marketing vision began in 2007 when Mylan Pharmaceuticals purchased the rights to the EpiPen brand inside a $6.6 billion packaged deal of 434 generic drugs from Merck Pharmaceuticals. Shortly after the acquisition, Mylan began increasing prices by increments of 10% per quarter until the EpiPen’s price had grown by over 600% in ten years that followed (Darden).

Mylan management defends the increases, claiming to have invested over $20 million in product and distribution chain improvements since acquiring the product (Koons). The firm’s executives cite that former owner Merck’s initial price of $94 per package generated a comparatively low 8.9% net profit in 2007. Defendants of the price increases also argue that price adjustments were necessary to create a sustainable supply chain of the lifesaving medicine (Lee).

The combined sum of those arguments were unable to pacify the critics after an investigative report by Ben Popkin of NBC news revealed that “from 2007 to 2015, Mylan CEO Heather Bresch’s total compensation went from $2,453,456 to $18,931,068, a 671 percent increase. During the same period, the company raised EpiPen prices, with the average wholesale price going from $56.64 to $317.82 per pen, a 461 percent increase, according to data provided by Connecture.” In a historical pricing perspective of the brand, Bresch’s salary increases alone increased the cost of manufacturing the EpiPen by nearly $5 per package; which, when contrasted to Merck’s original pricing, would have cost the product nearly its entire profit margin. The attention garnered by the compensation of CEO Bresch, along with the observation that over 40% of Mylan’s annual profits were now being generated by the EpiPen price increases, compounded Mylan’s public relations woes as a symbol of management’s greed, drawing nationwide criticism on executive pay excess and pharmaceutical anti-trust laws (Bastick).

Today Mylan has arrived at a strategic crossroads in its marketing vision. The firm’s 90% market share of epinephrine injectors will certainly be jeopardized if revised pricing fails to satisfy expectations of corporate responsibility, and the potential loss of the EpiPen market could cost stakeholders $847 million in annual earnings (Ubel). In addition, the brand collapse would generate a multi-billion dollar capital value loss of resale value of the brand. Since EpiPen’s patents will soon expire, Mylan’s original plan to sell off the division for a fast profit would be hampered by the devaluation of the EpiPen brand name, rendering the manufacturing facilities, goodwill and marketing capital worthless to prospective buyers.

Background

Unlike other pharmaceutical structure pricing bands, the EpiPen injector pricing was relative to the mechanical engineering patents contained within its dosing syringe system, rather than the chemistry of its medicine. The generic hormone solution inside the applicator has been widely available for years at prices less than $2 per dose; however, the precision, spring-loaded application syringes cost approximately $35 to manufacture. Critics claim that excessive marketing spending under Mylan’s management inflated the total cost to manufacture, market and distribute the device, from $80 to as much as $450 per package (Popkin). EpiPen had enjoyed a unique advantage in the drug market, because its mechanical design the EpiPen had been protected through engineering patents which were outside the pharmaceutical anti-trust regulations of the FDA (Darden). In addition, the arrival of new entrants to the market had been limited by the historically low profits earned by these injection devices (Lee).

The patents alone however, did not allow for a market domination, Pfizer had patented a rival product, the Adrenaclick, which was released for exclusive distribution through Wal-Mart in 2010. The new entrant, however, faltered due to limited brand awareness and its restrictive distribution exclusivity to Wal-Mart stores. In two years following its introduction, Adrenaclick failed to capture more than a 7% market share, despite selling at a price point of 1/3rd that of the EpiPens. In 2012 the maker of Adrenaclick sold off its manufacturing equipment and the product temporarily left the market, under the assumption that the timing was not right to continue challenging the EpiPen for market share (Bastick). Internationally EpiPen competed against a French rival the “Auvi-Q” which was sold in Europe at around $100 per package; however, Auvi-Q initially chose not to apply for U.S. distribution due to possible U.S. patent overlaps with some of EpiPen’s design. The continued existence of this international competition in the injector market remains the driving force behind why EpiPen prices in Europe have remained near their original 2007 prices, at around 1/5th the price of EpiPens sold in the U.S.

Much of Merck’s pre-2007 decisions for U.S. price points near the $100 mark were justified by the international price competition of the French Auvi-Q. Merck management believed that if U.S. market profits grew too lucrative, that Auvi-Q would challenge its U.S. patent rights, generating a legal battle that would cost years of EpiPen’s profits along the way. In addition to Auvi-Q, a new rival was introduced to the U.S. market in 2005 named Twinject which was marketed at a lower price point, at the time, than the $90 EpiPen. With pricing influenced by anticipated market competition of 2007, the 25 year old EpiPen line had been generating less than $17 million in profits from about $200 million in sales. Even Mylan executives had initially planned to spin off the EpiPen line from its new portfolio purchased in the Merck deal (Koons). However, CEO Heather Bresch saw a golden opportunity for the product and persuaded the board of directors to use EpiPen as a sample case for the future marketing of its generic brands. Mylan took on a revitalization marketing campaign and set its sights on capitalizing on the remaining untapped profits from its captive mechanical syringe market (Koons).

Pricing the EpiPen was a great challenge, since strategies in drug pricing are deeply complex; pharmaceutical makers are faced with a more complicated marketing landscape than manufacturers of retail goods. Prices for the same drug can vary widely from one country to the next, for example an EpiPen is priced in Great Britain at $69, in Germany at $190 and in the U.S. at $600. This variation among pricing processes reflects the complexities of distributing a product to meet a variety of competitors and price-influencing criteria in each market. For example in the U.S. the FDA along with private insurers utilize a market driven price allowance, in the spirit of capitalism, a drug maker can charge nearly any price for its products, a policy that is intended to draw new entrants into the market and drive prices down and quality up. In comparison, many European countries require an approved “reference pricing model”, which dictates the fair insurance reimbursement value of a drug is based on the costs of its alternatives. Some countries such as France include negotiable “price band” restrictions that cap the maximum price the drug can be sold at as an allowable percentage over the lowest price which the company sells the drug in other nations. Because of these price regulations some pharmaceutical firms choose not to distribute their products in highly regulated markets such as France and Switzerland (Rankin).

In 2009, the anticipated arrival of new entrants to the market became a reality when French rival Auvi-Q applied for North American distribution. Auvi-Q was expected to challenge EpiPens U.S. patent rights; however, Auvi-Q withdrew from the U.S. market entry after a series of safety recalls crippled their brand’s market value, they too believed the timing was not optimal to challenge the EpiPen for market share. Bresch’s strategy flourished by the subsequent delay of new competitors to the market and EpiPen found a growing market, even at much higher prices. The CEO’s belief was, that through an increased profitability of the mature market, Mylan had created an incentive for competitors to join with their own rival products in the final years remaining, until 2025, when the EpiPen patents would expire. The resulting lucrative margins created by the new higher prices would provide an improved resale market for the EpiPen division or the future licensing of its technology (Koons).

Mylan expected that the new players in the market would quickly drive EpiPen prices back to near its original $90 per package through price wars. During the eight year period of price increases, EpiPens previously stalled sales volume, even grew by 67%. Mylan had successfully expanded the existing market by lobbying for revisions to school medical restrictions which had prevented school staff from administering the shots to students in emergencies. With the restrictions lifted, Mylan further lobbied for tax subsidies to donate free EpiPens to schools, increasing goodwill and lowering corporate tax burden by $600 per package rather than the $100 per package deduction which would have been captured in the previous price formula. The theoretically deductible donations allowed Mylan to pay an effective 20% U.S. corporate income tax rate in 2015, saving it nearly $100 million in tax liabilities (Lee).

Bresch’s short-term strategy was directed at harvesting larger profits in the U.S. market through price increases, brand recognition and distribution expansion for several years until competitors could mobilize new products. From Bresch’s long term perspective, once that competition arrived to the market, Mylan could sell off the EpiPen brand and its soon expiring patent protection to the new competitors. However, in the eight years that followed the campaign launch, the anticipated competitive price pressure never materialized, as both Auvi-Q and Twinject suffered public relations problems and financial difficulties during the recession which caused both competitors to withdraw from the U.S. market by 2014. Capitalizing on the limited competition, Mylan increased prices by about 10% per quarter per year, gradually bringing the price from $90 per pair of EpiPens to over $600 per pair.

Alternatives

Mylan executives forecasted the introduction of EpiPen rivals by 2010, however the recession and other unforeseen regulatory factors delayed the arrival of that competition by nearly a decade. Bresch defends Mylan’s aggressive pricing strategy, justifying the tactics by capitalizing on the opportunity to harvest an additional $600 million per year in profits for every year that competition failed to materialize. Executives such as Bresch could claim a fiduciary obligation to the investors to exploit market gaps for shareholder gain and to pad the company cash reserves to fund new drug products (Koons).

In addition, Mylan leadership claims that they did not believe that they were creating a public safety crisis of affordability, because the allergic reactions could be just as effectively treated with an economical alternative which utilizes a $2 syringe and $5 vial of epinephrine. They pointed to the low switching costs of those alternatives and pointed to the examples of emergency responders that had converted back to dosing patients from syringes in addition to the arrival of free clinics which guided the uninsured on the creation of their own emergency kits for a fraction of the cost of a preloaded EpiPen (Rankin).

Mylan’s leadership could not have reasonably anticipated the market’s reluctance to self-dose from conventional syringes. Bresch initially believed that the primary competitive advantages envisioned for the EpiPen were limited to small children who could not administer epinephrine through syringes and to schools which were only protected from legal liability by using the EpiPen or an approved similar device (Koons). Regardless of price, consumer’s fear of incorrect dosing or injecting air into their bloodstream stalled the advancement of self-administered syringes (Bastick). The media scrutiny chose not to address that the EpiPen price should have little effect on affordable healthcare since it is viewed by medical practitioners as a simple convenience, rather than a medical necessity (Lee).

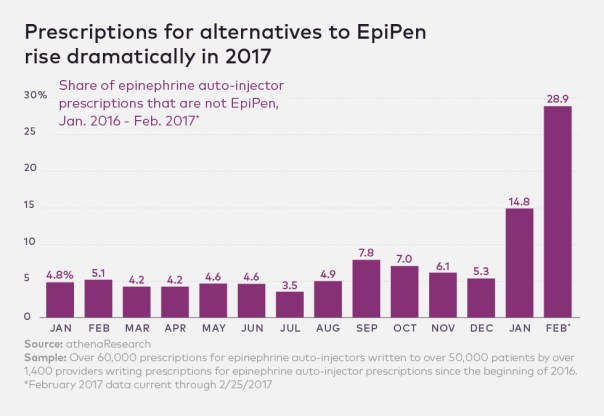

The lack of mounting competition for the past decade could not have been foreseen by management either, as three attempts at injector market entry by other firms failed due to poor timing or marketing. The introduction of a generic EpiPen competitor by Israeli firm Teva Pharmaceuticals was also denied by the FDA in 2016 further diffusing competitive influences. However, in late June of 2017, the FDA approved the next major player in the epinephrine injection market, Adamis Pharmaceuticals introduced their own injector under the brand name “Symjepi” a cheaper alternative to Mylan’s EpiPen, but expected to price higher the Adrenaclick (Bastick). Auvi-Q has also been approved to market their rival injector beginning in 2017 and Adrenaclick and Twinject have announced their returns to the market.

In response to consumer backlash and the coming arrival of generic substitutes, Mylan has announced that it will release a generic version of the EpiPen priced at around $300 per package of two. Analysts suspect that Mylan will continue to donate the EpiPen brand version to schools for a write off of $600 per package to maintain their tax savings and continue to promote the EpiPen brand to those whose insurance allows for brand name premiums. Despite the announcement, Mylan has not been quick to launch the distribution of its half priced generic alternative (Bastick).

Proposed Solution

The arrival of the new competitors, the aging patents, along with the media scrutiny makes a clear case for drastically reducing the EpiPen price. It stands to reason that competition among new firms will drive prices back down to the mid-$100’s per package or possibly even lower by 2025. The inevitable loss of EpiPen’s mechanical patent protection will soon render the brand’s competitive advantages obsolete. The EpiPen brand appears to have run its lifecycle and while the marketing tactics of Bresch succeeded at capturing an astounding quantity of remaining value from the brand; a change of course is needed to salvage the remains of Mylan’s public image and diffuse additional conflicts with lawmakers. The negative publicity around the EpiPen pricing is a driving force that pressured lawmakers to fine Mylan $465 million in 2016 for exploiting a regulatory misclassification to increase Medicaid reimbursement rates. It is likely that regulatory backlash will begin impacting the future FDA cooperation of Mylan’s other products. Continued friction between government regulators and Mylan could delay the FDA approval of more profitable new products and increase scrutiny into other areas of taxation and accounting regulations.

According to Porter’s five forces, over the next 10 years, EpiPen will suffer the fate of many other mature, low technology products which survived by the slight advantages of their distribution chain efficiency and became unable to grow and generate premium profits through technology advantages. For a firm such as Mylan, their interests would be best served by directing their focus toward the development of new products rather than expending administrative resources on the low-margin, maintenance of a supply chain distribution in a mature market.

Recommendations

Selling off the EpiPen brand and facilities to rival Teva Pharmaceuticals seems to be the most logical course of action. Teva’s acquisition of a widely recognized brand such as EpiPen would gain them access to the U.S. market which had recently been denied to them by the FDA’s rejection of their competitive product. The brand development value to Teva appears to exceed the future earnings potential of the EpiPen division to Mylan and could allow the firm to negotiate a premium sale price. However, there is some friction remaining between the leadership of both companies after Teva’s 2015 failed takeover attempt of Mylan.

The logical course of action, would be to advise Mylan’s CEO, Bresch, to contact leaders at Adrenaclick, Teva and Adamis to locate the highest bidder for the sale of the EpiPen brand prior to Mylan’s own launch of the generic version. By leveraging Teva’s offer, Mylan may be able to tempt either Adrenaclick or Adamis to pay a similar premium price for the brand. In addition, by delaying the generic marketing launch, a new competitor could capture the generic market by utilizing their own marketing campaign budget already allocated toward their entrance to the market. By allowing the new entrants to control the price band, the strategy could allow the entrants to more efficiently gain control over the adrenaline injector market, allowing the fewer remaining players to enjoy greater profit margins. It should be expected that EpiPen’s $800 million in annual profits will soon diminish back near the $18 million level of 2007 in the face of international competition and public scrutiny.

Conclusions

Mylan’s success at capturing untapped profit potential from a low-profit, mature market provided a valuable case study in both brand management strategies and an application of SWOT metrics. While the long-term brand potential remained limited, CEO Heather Bresch demonstrated great insight by capitalizing on EpiPen’s remaining market strengths and leveraged those strengths through marketing to exceed all foreseeable expectations of profit potential for the lackluster brand. Some analysts calculate that Bresch harvested more than three times the profits from EpiPen in the 10 years at the end of its patent protected lifecycle than the profits from all of the other companies combined, that owned the product along the 35 years that EpiPen was on the market (Koons).

The negative press would likely have been unforeseen by anyone, since the catalyst for the media scrutiny was originally aimed at Turing Pharmaceuticals and its outspoken CEO Martin Shkreli for their price hikes on lifesaving AIDS treatments. Mylan’s own negative press exposure was viewed by many as unjustified collateral damage, which brought an unfavorable spotlight on Bresch’s strategy and may have accelerated the entrance of new competitors which had been waiting patiently to exploit the optimum timing to reduce switching costs for consumers (Lee).

The public relations opportunity that Mylan probably missed was to demonstrate an empathy toward the uninsured by launching a parallel campaign to provide a package of free EpiPens a year to the uninsured or low-income underinsured customers, rather than their chosen direction of providing “$100 off” coupons that were limited only to those with commercial health insurance. Mylan’s disregard for the underinsured struck a nerve with the low-income masses and fueled the media frenzy that surrounded the executive pay scandals. The public relations damage to Mylan’s brand value and the resulting lack of political cooperation that will follow could be estimated to cost several billion dollars in the coming years as lawmakers begin to apply their own pressure by withholding cooperation and avoiding any compromises that appear to benefit Mylan.

Exhibit 4. Expert Financial Analysis

Martin Zweig Analyst Commentary on Recent Financial Performance of Mylan: Guru Score 62%

P/E RATIO: [PASS] The P/E of a company must be greater than 5 to eliminate weak companies, but not more than 3 times the current Market P/E because the situation is much too risky, and never greater than 43. MYL’s P/E is 38.62, , while the current market PE is 19.00. Therefore, it passes the first test.

TOTAL DEBT/EQUITY RATIO: [PASS] A final criterion is that a company must not have a high level of debt. If a company does have a high level, an investor may want to avoid this stock altogether. MYL’s Debt/Equity (128.91%) is not considered high relative to its industry (152.29%) and passes this test.

SOURCES

“10 New Years Resolutions for the Pharmacy Industry”. 2017. Medreps.com

https://www.medreps.com/medical-sales-careers/10-new-years-resolutions-for-the-pharma-

industry/

Bastick, Erin. 2017. “EPA Approves EpiPen Rival”. Formulary Journal.

http://formularyjournal.modernmedicine.com/formulary-journal/news/fda-approves-epipen-rival

Lee, Jaime. 2016. “Mylan CEO defends EpiPen strategy, questions pricing model in the U.S.” MMM

Online. http://www.mmm-online.com/commercial/mylan-ceo-defends-epipen-strategy-questions-

pricing-model-in-the-us/article/576448/

Koons, Cynthia. (2015). “How Marketing Turned EpiPen into a Billion Dollar Business”. Bloomberg

Business Week. https://www.bloomberg.com/news/articles/2015-09-23/how-marketing-turned-

the-epipen-into-a-billion-dollar-business

Mattingly, Joseph. 2017. “Drug Price Wars, Episode VII: The General Assembly Awakens”. Mattingly

Report. https://www.mattinglymanagement.com/2017/02/generalassemblyawakens/

Popkin, Ben. (2016). “Mylan’s CEO Pay Rose over 600% as EpiPen Prices over 400%”. NBC News. http://www.nbcnews.com/business/consumer/mylan-execs-gave-themselves-raises-they-hiked-epipen-prices-n636591

“Pricing the EpiPen: This is Going to Sting”. (2016). Darden Business Publishing University of Virginia.

https://cb.hbsp.harvard.edu/cbmp/product/UV7186-PDF-ENG

Rankin, Peter. 2014. “Global Pricing Strategies for Pharmaceutical Product Launches”.

http://www.pharmaceticalpricing.com Sourced:

https://www.crai.com/sites/default/files/publications/Global-Pricing-Strategies-for-

Pharmaceutical-Product-Launches.pdf

Ubel, Peter. 2017. “What is Maddening About Pharmaceutical Prices”. Forbes.

https://www.forbes.com/sites/peterubel/2017/04/28/what-is-maddening-about-pharmaceutical-

prices/2/

Zweig, Martin. 2017. “Mylan Guru Performance Assessment”. NASADQ.

http://www.nasdaq.com/symbol/myl/guru-analysis/zweig#anchor2

Reblogged this on Todd Benschneider.

LikeLike